All Issues

Rural Latino families in California are missing earned income tax benefits

Publication Information

California Agriculture 58(1):24-27. https://doi.org/10.3733/ca.v058n01p24

Published January 01, 2004

PDF | Citation | Permissions

Abstract

When properly accessed, the federal Earned Income Tax Credit (EITC) can boost a family's yearly income by more than $4,000. A study in Kern and Madera counties indicated that many, perhaps most, qualified low-income Latino families living in rural California communities may not be receiving the EITC. About 80% to 86% of eligible households nationwide receive the EITC, compared with about 36% of eligible California families in the study. The primary reason appears to be lack of accurate information and limited access to tax-preparation assistance. UC Cooperative Extension advisors and staff are well situated to provide information about the EITC.

Full text

Tax-preparation services are often limited in rural communities.

The federal Earned Income Tax Credit (EITC) can boost a low-income family's yearly income by more than $4,000. The credit aims to reduce poverty, promote work and help families build assets.

The Earned Income Tax Credit (EITC) has been described as the largest and the most successful federal assistance program for low-income working families with children. When properly accessed, it can boost a family's yearly income by more than $4,000. More than 16 million U.S. low-income families received $30 billion from this income supplement in tax year 2001. In 2001, the EITC elevated the families of 5 million children above the federal poverty line (Berube and Forman 2001). Implemented in 1975, the credit reduces poverty, promotes work, reduces income inequality, helps low-income families to build assets and encourages flexible resource utilization (Wirtz 2003; Cauthen 2002).

The original objective of the EITC was to offset payroll taxes, which disproportionately affect lower-income workers, and to supplement wages, encouraging work participation (Phillips 2001). Eligible families — those with incomes below 200% of the federal poverty line — that do not file for and receive the EITC are missing a valuable resource.

A unique characteristic of the EITC is its refundability. Eligible working parents are refunded any amount that remains after the credit offsets the worker's tax liability, or can receive the full amount of the credit if they had no tax liability. Married workers with one qualifying child who earned less than $30,201 in tax year 2002 received up to $2,506 in additional income. Low-income married workers with two or more children, who earned less than $34,178 in 2002, were eligible for up to $4,140. Passage in 1996 of the federal Personal Responsibility and Work Opportunity Reconciliation Act, better known as “welfare reform,” increased the importance of the EITC as a work incentive and wage supplement for the many families who were moved off welfare support to work in the low-wage sector (Greenstein 2002).

Who receives the EITC?

More eligible families receive the EITC than any of the traditional transfer programs, such as TANF (Temporary Assistance for Needy Families), Medicaid or food stamps. However, certain groups of qualified workers file for and receive the credit less often, including households with very low incomes, former welfare recipients and workers who speak a language other than English (Berube and Forman 2001). According to the 1999 National Survey of America's Families (NSAF), low-income Latino families nationwide are the least likely to know about or to ever have received the EITC (Phillips 2001). Approximately three-fourths (74%) of low-income, non-Latino NSAF participants had heard of the EITC and about 50% had ever received it, whereas only about 32% of Latino parents knew about the credit and only 18% received it.

Moreover, despite the prevalence of low-income families in rural communities, the bulk of the EITC goes to urban and suburban workers (Berube and Forman 2001). Proportionately little of the credit makes its way to workers in remote locations. The rural locale itself may contribute to this skewed distribution by providing residents with less information about and access to programs that support work and enhance well-being.

We studied Latino low-income rural families in Kern and Madera counties, to develop quantitative data about usage of the EITC and qualitative information describing factors that affect access to the credit. We found that many, perhaps most, of these families were not receiving the EITC. About 80% to 86% of eligible households nationwide receive the EITC (Burman and Kobes 2002), compared with about 36% of eligible California families in our study.

Rural Families Speak Project

The Rural Families Speak Project (2004) is a multistate, longitudinal study currently in its fifth year, which is assessing changes in the functioning and well-being of rural families in the wake of welfare reform and associated reductions in programs and services. Beginning in 2000, researchers from 15 universities including UC began gathering annual qualitative and quantitative information about participants' financial and family well-being and program participation during intensive one-on-one interviews with mothers having at least one preschool-age child. A total of 414 interviews were conducted in the 15 participating states in 2000. We report on findings from this first wave of data collected from the California sample, and examine reported receipt of the EITC for the previous tax year (1999).

We interviewed 35 low-income Latino mothers living in rural Kern and Madera counties. Participating mothers were recruited through subsidized day-care programs and by word of mouth in three Central Valley communities, Delano, Wasco and Madera. Each family had a child of preschool age and was eligible for (although not necessarily receiving) food stamps or vouchers through the Supplemental Nutrition Program for Women, Infants, and Children (WIC).

A survey of rural California families was conducted as part of the Rural Families Speak Project, a multistate effort to evaluate the impacts of welfare reform. Above, Martha López interviews a mother one-on-one about her family's financial status at the UC Cooperative Extension office in Madera County.

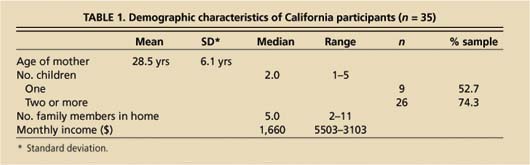

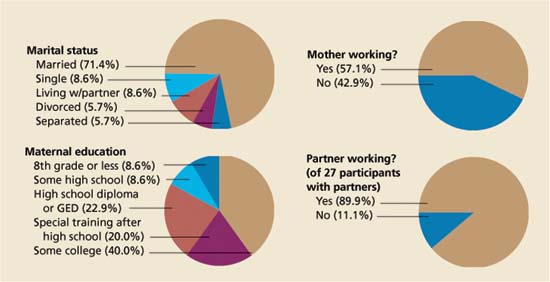

Latino mothers in the California sample averaged 28.5 years old (table 1; fig. 1). The majority were married or living with a partner (80%) and had two or more children (74.3%). Families often had one or more additional family members living with them. Participating mothers tended to be well educated. The majority of families also included at least one working parent. At the time of the first interview, 57.1% of the mothers and 89.9% of their partners were employed in low-wage work. The median family income was $1,660 dollars per month, just under the poverty threshold for a household of five with two young children (US Census Bureau 2000).

Rural Latino families and EITC

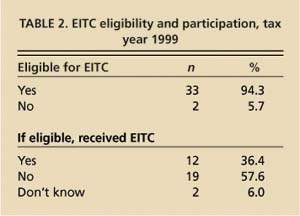

In order to be eligible for the EITC in 1999, workers had to be legal residents of the United States; earn wages during the tax year; have one or more natural or legally adopted children, legally placed foster children or stepchildren under age 18 living in the home; and have income less than 200% of the poverty threshold. According to these criteria, 33 of the Latino families in the study were eligible to file for and receive the EITC (table 2).

However, only 36% of the eligible rural California study subjects (n = 35) actually filed for and received the EITC in the previous tax year. The majority of the eligible families (between 58% and 64%) failed to take advantage of the income supplement. About 85% of eligible families benefit from the EITC nationally. It appears that our findings — which indicate that significantly fewer eligible low-income Latino families living in rural California communities receive the credit — are supported by similar findings at the national level.

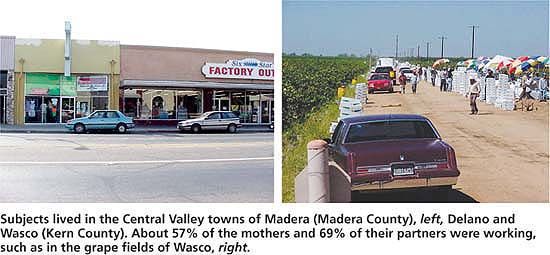

Subjects lived in the Central Valley towns of Madera (Madera County), left, Delano and Wasco (Kern County). About 57% of the mothers and 69% of their partners were working, such as in the grape fields of Wasco, right.

The qualitative data obtained by indepth interviews provided insight into the issues affecting the use of the EITC by eligible families. Lack of or inaccurate information about the existence of, eligibility for and filing procedures was common. Language and cultural barriers further diminished the likelihood that Latino families knew about and accessed the credit.

Most eligible families in the study who were not receiving the EITC were unaware of its existence and applicability to their family situation. One mother gave a typical response. “I don't know about that,” she said. “I think we always had to pay [taxes].”

Furthermore, study subjects who had heard of the EITC often had inaccurate information about how it works and their eligibility. Low-income workers often do not file a tax return when they believe they do not owe taxes or will not receive a refund. The refund-ability of the EITC means that eligible workers can receive the amount of the credit that remains over and above their tax liability — or the total amount of the credit if they owe no taxes. However, in order to receive the credit, workers with or without tax liability must file a federal return that includes specific paperwork (Schedule EIC).

Typical responses indicated that many subjects did not understand how the credit works. A 19-year-old mother stated, “You have to be a certain age, I think, to get that.” In fact, the small EITC available to single, low-income workers without children is not available until the worker is 25 years old. There are, however, no age requirements for working parents with children who qualify — as long as the worker is not claimed as a dependent on their own parent's tax return.

Often participants eligible for the EITC failed to file because they believed it was too much trouble or only applicable if they had tax liability to offset. These mothers understood that by filing income tax forms (such as the 1040EZ) with Schedule EIC they could receive a refund that included an amount of money over and above withheld taxes. But one typical participant said, “I don't file taxes. That's nothing but a hassle.” Furthermore, legal immigrant workers who are unfamiliar with the system or have language barriers and reduced access to qualified tax-preparation help may not understand that they are eligible for the EITC, even if their immigration status makes them ineligible for other public benefits.

Location, cultural and language issues, as well as limited education, may contribute to lack of knowledge and usage of the EITC. The isolation of rural areas (Fisher and Weber 2002) and possible linguistic isolation of Latino families may prevent adequate information from reaching qualified workers. In addition, research on strong cultural ties, utilizing the Michigan data from the same national study, identified the immediate and extended family as the main source of assistance and support. These strong ties limit efforts to access assistance from informal sources of support or contact with agencies and community resources.

Although programs that disseminate information about the EITC and encourage and assist eligible workers have been successful in metropolitan and suburban areas (Fleischer and Dressner 2002), there has been little effort to assist rural, low-income, multicultural workers.

Only about 36% of the surveyed families who were eligible for the EITC applied for and received it in 1999. Outreach in rural communities is needed to ensure access to this important benefit for low-income workers and their children, above.

Families living in urban areas have access to agencies that provide information on EITC as well as free tax-preparation assistance. Many of these agencies do not have offices in the small rural communities where the Latinos live. All of the 22 tax-preparation offices in Madera are for profit. The only free service is provided at the Madera County Library on a first-come basis. In Kern County, there are few tax preparers in Wasco (one) and Delano (seven), while free tax-preparation services are provided in Bakersfield, the county seat 30 miles south. Even if an urban area is only a few miles away, rural low-income families often do not have cars and their access to public transportation may be limited. Often a family member voluntarily prepares income tax returns for multiple family members. While the family values this assistance, usually that individual is untrained in tax preparation and only uses the short form (IRS 1040EZ).

The Internal Revenue Service (IRS) recognizes that the EITC is underutilized by limited-resource families in rural areas and is looking for ways to improve outreach. One model, developed by Georgia Cooperative Extension, relies on active involvement of Cooperative Extension staff in providing information and offering free tax-preparation assistance (M. Rupured, University of Georgia, personal communication, 2003).

How can EITC access be improved?

Merely providing accurate information about the EITC may greatly increase usage by eligible families. IRS-provided information flyers about the EITC were sent to research participants in California after the first-year interviews. At year two, it appears that the percentage of eligible families who received the credit more than doubled.

Even when qualified workers file for and receive the credit, several factors can interfere with their receipt of the maximum amount of money for which they are eligible. Tax-preparation and loan fees are eroding the benefits of the EITC. Many low-income workers who believe they would not be able to accurately prepare their federal and state tax returns go to preparers who charge as much as $100. In addition, many of these preparers encourage clients to get the money right away by taking out a refund anticipation loan (RAL) with fees as high as $90 to $300 (Kim and Berube 2003). As a result, in 2002 about $2 billion that was intended to benefit low-income families went directly to commercial tax preparers and affiliated national banks (Kim and Berube 2003). Programs that provide free or low-cost tax-preparation assistance, encourage and assist low-income workers to obtain bank accounts (for faster electronic refunds from the IRS) and promote consumer awareness about the extreme costs of RALs can reduce these tendencies and decrease out-of-pocket tax-preparation costs (Kim and Berube 2003).

Our study findings clearly indicate the need for informational programs that reach out to rural communities, providing accurate information about the existence of the tax credit, eligibility, tax-preparation procedures and availability of low-cost or free tax-preparation assistance. Each year the IRS provides good bilingual information regarding the EITC in an effort to reach eligible families. Currently, EITC information is being included as part of many Expanded Food and Nutrition Education and Food Stamp Nutrition Education program efforts in California. Unfortunately, these programs do not have the capacity to reach all rural areas. To provide increased coverage, UC Cooperative Extension's Spanish Broadcast and Media Services provides this information in written and oral formats. Providing the information helps increase the number of families utilizing this credit. The challenge is to utilize our many networks to reach Latino families in rural areas.

Underutilization of all public resources was a notable trend among the study participants. The lack of usage of the EITC may be just another example of how Latinos in rural areas are not accessing available resources. While providing information on the EITC will help, improving overall access to public benefits for limited-resource Latinos is a larger issue that must be addressed.

Rural Latino families in California are missing earned income tax benefits