All Issues

Free trade impacts: Mexico's tomato processing industry may gain

Publication Information

California Agriculture 45(5):11-14.

Published September 01, 1991

PDF | Citation | Permissions

Abstract

The tomato processing industry has expanded more rapidly in Mexico than the fresh tomato industry. Export of tomato paste to the United States has doubled since 1986 and will increase still further when the US. tariff is eliminated under the Free Trade Agreement (FTA). This will permit Mexico to displace other suppliers to the U.S. market (such as Chile, Turkey and Taiwan). It will probably cause lower prices for U.S. producers as well. (Editor's note: Most tonnage statistics in this paper are in metric tons. In a few cases, U.S. tons have been used, and so designated. For conversion purposes, 1 metric ton = 2,205 lb; 1 US. ton =2,000 lb.)

Full text

Tomato production in Mexico is an important component of Mexico's agricultural production and more particularly, of its agricultural exports. Most of the output is destined for fresh markets in Mexico and the United States; about 20% is used for processing. In 1989, for example, 947,000 metric tons (mt) were shipped to domestic fresh markets, 361,000 mt were exported, and another 318,000 mt were processed in Mexico. Fresh tomatoes account for 10% of total agricultural exports and are the first or second most valuable export, depending on the year. Processed tomato products account for less than 1% of these exports. This disparity is reflected in U.S. imports from Mexico during the same year: ĉ223 million for fresh tomato imports and ĉ17 million for processed.

However, during the 1980s the tomato processing sector grew much more rapidly than the fresh sector in Mexico and almost three times as fast as the processing sector in the United States. Despite this change, most attention in the United States has focused on competition in fresh tomato markets and how it might be impacted by the proposed North American Free Trade Agreement. The purpose of this report is to give similar attention to the processing sector. Currently, tomato paste producers in the United States enjoy the protection of a 13.6% import duty paid on Mexican tomato paste.

The results reported here are based on data collected from Mexican and U.S. sources, as well as interviews conducted with two California processors and with the Mexican National Vegetable Producers Association (Confederation National de Productores de Hortalizas, or CNPH). The latter is comprised of five Mexican processing firms that account for almost 75% of the country's installed paste capacity. Interviews were conducted in Sinaloa, where the processing industry is concentrated, during the week of April 8,1991. CNPH was very helpful in arranging interviews and the processors cooperated fully in providing information and opinions about their industry.

Field research was conducted in the state of Sinaloa, which dominates tomato paste production in Mexico. Sinaloa produced 1.1 million metric tons (mt) of tomatoes from 73,000 acres (29,450 hectares) in 1989. Close to 30% of that, or 317,000 mt, was delivered to processors.

Production and exports

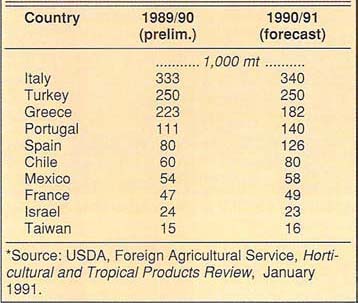

Mexico produces tomato paste and derived products almost exclusively. The output and export of other processed tomato products such as canned tomatoes is very small and not significant for purposes of this report. Mexico ranks eighth among the worlďs producers of tomato paste (table 1). According to U. S. Department of Agriculture (USDA) forecasts of 1990-91 paste production by non-U.S. producing countries, Mexico's expected output of 58,000 mt was less than 20% of that produced by Italy, the leading non-U.S. producer.

The U.S. processed tomato industry no longer reveals its production levels. If the relationship of California's paste production to total production was the same in 1990 as in 1983-85, then the California production of paste in 1990 would have been about 773,000 mt, 14 times as great as in Mexico. (Calculations were made from published data and industry survey results; 58.7% of all tomatoes sent to processors from 1983 to 1985 were used in tomato paste production.)

Another indication of relative industry size is the volume of tomatoes delivered to processors in 1990:365,000 mt in Mexico and 8.4 million mt in California.

Mexico's position as a supplier of processed tomato products to the U.S. market varied between 1986 and 1990. The volume grew each year, rising from 13,492 mt in 1986 to 26,320 mt in 1990. This growth paralleled the expansion in Mexican paste production that occurred during the same period. Mexico's share of the value of all U.S. imports of processed tomato products ranged from 8.8% to 16.5% (table 2). Most of the trade results from open negotiations although some is accounted for by intrafirm transfers or long-term contractual arrangements. All of the output of Sinaloapasta, which accounts for 15% of installed capacity, is exported to the account of its parent company, Campbelľs Soup, At least one other processor exports significantly for the account of its U.S. affiliate.

TABLE 1. The production of tomato paste, 28-30 Brix basis, in producing countries except the United States, 1989-90 and 1990-91*

Mexico's competitive potential

An industry is competitive if it can obtain and maintain a profitable share of the market for its product. Its ability to do so depends on prices and costs relative to those of competitors, alternative opportunities, access to markets, management skills, and the adoption of appropriate technology.

Costs

Raw product costs in Mexico are highly dependent on prices for fresh market tomatoes. One processor reported paying from $80 to $100/mt for tomatoes in 1990 and from $43 to $50/mt in 1991. Another reported that prices were $15/mt less in 1991 than in 1990. Large supplies of fresh market tomatoes caused prices to drop and increased the quantify diverted to processing use. When fresh market prices are high, industrial varieties are attracted to that market regardless of contracts with processors. Processors contend that contracts are difficult to enforce, so that expected prices and supplies are not always achieved.

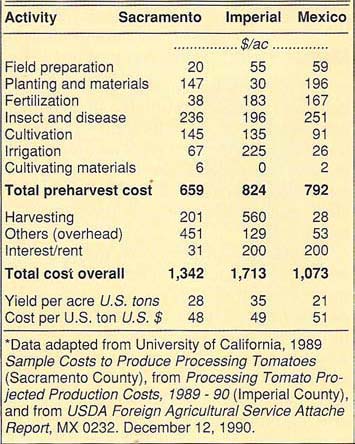

Tomato prices do not necessarily cover costs of production. A comparison of two cost estimates, one made by UC for California producers and the other by the U.S. Department of Agriculture (USDA) for Mexican producers, shows that production costs per ton in California and Mexico are relatively close in value. UC estimated production costs for processing tomatoes in 1989 in Sacramento and Imperial counties. The USDA classified costs into different categories than did University researchers. Therefore, we reclassified the University cost estimates to be compatible with those published by USDA. This process caused the California costs to be slightly different than those published by UC. When the costs in Mexico and California are compared, they show the greatest differences in harvesting, overhead, irrigation and interest charges (table 3).

TABLE 3. Costs for producing tomatoes for processing, Sacramento and Imperial counties, California and Sinaloa, Mexico, 1989*

The harvesting cost estimate for processing tomatoes in Mexico, as published by the USDA, is $28/ac or $1.33/U.S. ton. This figure doesn't appear to be plausible. Two processors in Mexico estimated that harvest costs ranged from $8.50 to $12.50/ U.S. ton. UC estimated that harvesting costs were $7 and $16/U.S. ton in Sacramento and Imperial counties, respectively. (Harvesting costs per U.S. ton are derived from table 3 data by dividing harvesting costs per acre by yields per acre, or $201 and $506 by 28 and 35 tons, respectively.) It may be that the labor hours used in harvesting were allocated to preharvest activities in error or due to an unknown accounting method. In any event this remains an area of uncertainty concerning Mexican production costs.

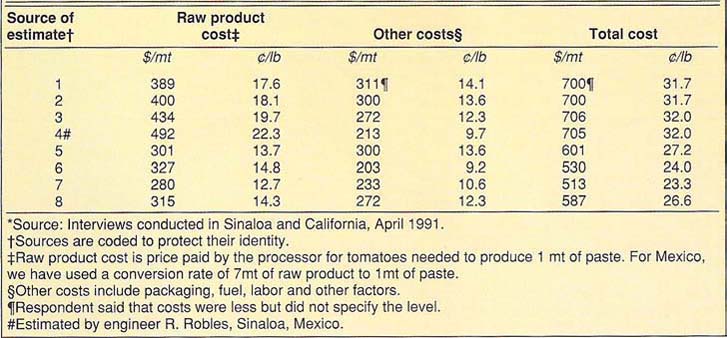

The costs for producing tomato paste in Mexico vary among processors. Eight estimates were derived from information provided during interviews in Mexico and California. They are summarized in table 4. The costs varied because of different raw product costs, plant efficiencies and accounting methods. They ranged from 23.3 to 32¢/lb at the plant, with corresponding duty paid costs at the border of about 30 to 40¢/lb.

I constructed a sample cost of processing from these estimates based on a budget spread sheet using input costs from the interviews. Typically, Mexican processors obtain 1 mt of paste from 7 or more mt of raw product. (This is 1 mt more raw product than is required in the United States, where the ratio of raw product to paste is 6:1. The difference is largely due to varietal differences in tomatoes: U.S. processing tomatoes tend to be higher in solid content than Mexican tomatoes.) The ratio of 1 mt paste derived from every 7 mt of raw product in Mexico is used in the following calculations.

Using an average cost of $45/mt for raw product in 1991, the raw product cost per metric ton of paste is $315 ($45 x 7 mt).

Other costs for paste production (including direct costs such as labor, packaging, and fuel, and other overhead and financial costs) were estimated to be $253/mt. Total cost was $568/mt or 25.8*/lb. This could result in a duty paid cost at the U.S. border of 33¢/lb, 3 to 4¢/lb lower than my estimate of about 37¢/lb, free on board (f.o.b.) plant cost, for California processors specializing in paste production. This estimate was derived from interviews with three processors and others familiar with industry production practices. Since freight charges from California to midwestern and eastern markets are approximately the same as they are from the Mexican border, delivered costs for most Mexican paste are likely to be 3 to 4¢/lb lower than these California costs.

These costs are not always recovered through market prices. Fancy tomato paste (31° Brix or 31% soluble solids, a measure of sugar content by weight) sold at prices at or below 36°, f.o.b. California plant, in May and June 1991 with some selling at 34° and perhaps small quantities at lower prices. These prices are below my estimate of average California costs, but are still attractive to some Mexican processors.

If the U.S. duty of 13.6% on the value of imported paste were removed, the landed cost of paste from Mexico would drop about 3.5 to 4¢/lb to a likely level of 29 or 30¢/lb at the border (based on $45/mt tomatoes). This would increase Mexico's cost advantage relative to paste produced in California to 7 or 8¢/lb (equivalent to $25 per U.S. ton for tomatoes).

Because the costs of producing tomato paste vary among Mexican producers, we might alternatively assume a cost of $90/t, changing the picture significantly. If the tomato price increased to $90/t in Mexico that would add 15.5¢/lb to the Mexican production cost and increase their cost to a level above that of many U.S. processors (25.8¢/lb + 15.5¢/lb = 41.3¢/lb).

Prices

Two scenarios are of interest in regard to lower import prices. One is the situation in which import duties are eliminated for all paste imports, as might occur under a General Agreement on Tariffs and Trade (GATT) settlement. The other is the situation under a negotiated North American Free Trade Agreement in which tomato paste from Mexico gained duty free entry to the United States, but other paste did not. To evaluate the impact of lower prices on shipments of tomato paste, it is necessary to analyze how demand has responded to price changes in the past. In a 1982 article, UC Davis Professor Ben French and colleague John Brandt estimated the sensitivity of prices to changes in supply. Their estimated price flexibility of demand for tomato paste was -0.4131, which means that a 10% increase in paste supply would create a 4.1% reduction in price, other things held constant. This suggested that a 10% reduction in price is likely to stimulate a 24% increase in shipments. A drop in tariffs might induce a price decline of 4° in paste prices (the amount of the tariff on paste with a customs value of 29¢/lb), which is approximately 10% of recent prices. If California prices dropped to match this level so that the average of domestic and import prices was down 10%, then total shipments (imports and domestic) would go up about 25% to meet domestic demand requirements. However, high cost producers in California and elsewhere would cut or eliminate production in the face of persistently lower prices and the market share of lower cost producers like Mexico would increase.

A more likely outcome is that prices would reach some “equilibrium” level below current levels but above the full amount of the tariff decline. In such a case, California processors would lose market share and profits and foreign suppliers would gain them. An important caveat to this scenario is that if such a GATT settlement was reached it should require a dismantling of European Community (EC) subsidies for tomato paste. The net result would be little change in the landed cost for EC produced paste and a shift in demand toward Mexico, Chile and other suppliers with lower costs.

If a 4¢/lb reduction in landed cost was achieved by Mexico alone, the' case under a free trade agreement, Mexico's share of the U.S. market would increase. I don't know the amount of change because I have been unsuccessful in estimating the price elasticity of demand for Mexican imports. Based on the elasticity estimate discussed above for all imports, it is reasonable to expect that imports from Mexico, the only supplier with a lower cost, would increase by more than 25%, other things being equal. Import market share would be gained against Chile, unless Chile were able to further reduce production costs. Other losers in the import paste market would be Brazil, the EC, and Israel.

U.S. producers would lose market share and profits also. Lower costs for Mexican processors would generate higher profits that would stimulate further investment in the industry and expanded output and exports. The additional supplies on the U.S. market would lead to lower prices. For example, if added imports increased U.S. supply by 10% and if French's estimate of a price flexibility of -0.4131 still holds, then a 4% reduction in U.S. prices would be expected. As Mexican exports continued to expand, higher-cost processors in the United States and Mexico would need to find alternative markets or leave the industry. The impact would be greater if prices fell by the full amount of the tariff reduction, as noted above, and would be less severe if the demand for tomato paste grew more rapidly than supply. However, at least one U.S. processor reports that the rate of growth in paste demand slowed in 1990-91 and is inadequate to sustain current production potential at profitable levels.

Workers sorting tomatoes in one of Hunt-Wesson's California processing plants.

If the Mexican price dropped by 10% due to liberalized trade, and U.S. prices met this price reduction, the U.S. demand would grow by 25% (the demand elasticity of -2.5 is implied by the French and Brandt price flexibility estimate of -0.4131). Mexico would likely capture a major share of that growth because of its low cost of production. Unless constrained by currently unknown factors, Mexican exports to the U.S. would increase by more than 25%.

The estimates of import changes are based on a one-time change in price equal to the full amount of the U.S. tariff reduction and on immediate response by import suppliers. They assume that other factors remain as they were. In fact, duty reductions, if they occur, are likely to be phased in over several years (10 years in the case of Israel) and import prices may not decline by the full amount of the tariff reduction. Both the domestic and foreign industries will adjust their production and marketing decisions throughout the period. However, as has been observed in the case of the frozen broccoli industry, if the basic economics of production favor Mexico, if market access is achieved, if product quality is consistent with market requirements, and technology levels are competitive, then Mexico's share of the U.S. tomato paste market will increase and California's will decline. This will increase investment and employment in Mexico and decrease them in California.

Alternate opportunities

The major competition for processing tomatoes in Mexico is fresh market tomatoes. Tomato producers may sell to the fresh market or the processing market depending on prices. This situation makes it difficult for processors to forecast their output and establish efficient delivery schedules. These alternatives are viable because contracts for processing tomatoes are difficult to enforce (the legal system works slowly and laws are not precise). Processors may pay whatever price is needed, sometimes on a week-to-week basis, to attract product away from the fresh market. This occurred in 1990-91, when fresh market export prices rose to 52¢/lb from a price of 27¢/lb a year earlier. Processors had to pay up to $80/mt to obtain product for processing. In 1990-91, the fresh export price dropped back to 27¢/lb and processing prices fell as low as $33/mt, but averaged closer to $45/mt.

This relationship between the fresh and processing markets for tomatoes impedes the development of the Mexican processing industry because it creates supply and pricing instability. Paste production expanded in Mexico by taking an increasing share of the country's total tomato production, but at the same time it remained vulnerable to changes in fresh market demand. This is reflected in the highly variable costs for paste. Increased specialization in producing tomatoes for the processing industry would probably stabilize costs, stimulate the adoption of efficient processing varieties, and facilitate improved management of raw product supplies. This is the basis for the industries in California and Chile, for examples.

Access to markets

Mexico's paste industry has good access to U.S. markets because of its proximity to the United States and the links that at least two major processors, Sinaloapasta and Productos Industrializados del Fuerte, have with U.S. processors. I have not evaluated the marketing programs of Mexican processors, but believe that the high proportion of production that is exported to the United States and the recent growth in paste exports indicates that market access is not a problem.

Management skills and technology

It is difficult to separate these two factors because good management generally leads to the adoption of appropriate technology. Plant management and processing technologies appear to be good. Under-utilization of plant capacity appears to be a consistent problem. This reflects some inefficiency in planning and plant operation, but is more of a problem in field management. According to one interview, repair and maintenance is hampered by the lack of easily accessible parts and repair experts. This is a manifestation of an inadequately developed infrastructure to support processing operations.

I am less certain about the management of tomato production. The persistence of low yields and the scheduling problems cited by processors suggest that field management and technology can be improved. If this were to happen, capacity utilization would increase and unit costs would decline. Improvements in technology and management would lower tomato production costs, which, on a per-ton basis, are close to those in California. If such changes were reflected in lower tomato prices they would improve the competitiveness of Mexico's processors.

Overall assessment

Mexico is capable of landing tomato paste in United States at a cost lower than California's cost of production. This capability is not always realized because raw product costs are highly variable. For example, Mexican landed costs in 1990 were comparable to California, but those in 1991 were lower. The industry's competitiveness is hampered by the price and supply uncertainties created by its link to fresh markets. It could be improved by better management of raw product supplies. Water and labor availability do not appear to be constraints on the processing industry but a lack of capital may have discouraged much expansion. Pests and disease present problems periodically but seem to be manageable. However, if U.S. regulations on chemical use are changed or force more stringent controls in Mexico, then pest control could mean added costs for the industry.

Conclusion

Mexico is a strong competitor in the global market for tomato paste. Its cost levels are low relative to the United States and it is closer to the U.S. market than other major suppliers. Changes in industry profitability through a reduction in the U.S. tariff or a reduction in Mexican costs will stimulate price reductions and an increase in Mexico's share of the U.S. market at the expense of California and other high-cost producers serving the market.

Future investment in the Mexican processing tomato industry will be strongly influenced by improvements in economic stability, a lowering of the U.S. tariff on tomato paste, and a stabilization of the raw product supply. It will be sensitive to changes in technology that alter the competitive balance between Mexican and other producers, to improvements in management skills, and to improvements in the input and transportation services to the industry. Increased investment by U.S. food processing firms might strengthen marketing links to the United States and facilitate a more rapid rate of technological adoption. Improvements in economic stability include stable and reasonable inflation, interest and exchange rates, and consistent and equitable public policy.

Development of the industry will be linked to that of the fresh market sector. If the demand for fresh tomatoes continues to grow, then the processing industry will face continued competition for raw product and will face periodic supply and price problems. To the extent that the industry is able to develop and keep its own raw product base, then pricing and supply will become more stable and this should lead to improved management practices and better yields. If fresh market demand slackens, then the industry may find low tomato prices as the surplus seeks a home.

Mexico has a production cost advantage over U.S. producers because of low labor costs. However, the advantage is not as great as it would be if yields and conversion rates were better. Reduced tariffs into the U.S. market and improved economic stability will stimulate added investment. This could lead to better raw product management which would increase capacity utilization and lower unit costs. Increased productivity could result in lower raw product costs, reducing a problem currently facing the industry. A limitation on expansion may be increasing Mexican labor costs due to wages rising more rapidly than productivity. Mexican cost advantages might also be partially offset by changes in regulations concerning chemical use and worker safety.

The timing of new investment will depend on the course of paste prices in the international market. Prices in July 1991 were below costs for many processors and certainly not attractive for new investment. Prospects for large paste supplies in 1991-92 are also likely to restrain investment. It may well be that by the time that the economic situation stabilizes and tariff negotiations are completed, tomato paste prices will be on the upswing. Further investment is unlikely until after 1992. Such investment will create a marked change in Mexico's efficiency and costs. Industries in California, Chile, and other regions supplying the U.S. market will need to make adjustments to meet such a change in Mexico's competitive status.

Free trade impacts: Mexico's tomato processing industry may gain